Civil society from borrowing and lending countries call for new approach to assessing debts

The IMF and World Bank are reviewing the Debt Sustainability Framework, their main policy which is meant to prevent debt crises in the most impoverished countries. Over thirty civil society organisations have outlined a set of major changes which are needed to address failings of the current system. As well as Jubilee Debt Campaign, authors of the statement include the African Forum and Network on Debt and Development (Afrodad), Red Latinoamericana sobre Deuda, Dessarollo y Derechos (Latindadd) and the European Network on Debt and Development (Eurodad).

The groups’ demands include moving assessment to be conducted by an independent but accountable UN organisation rather than the IMF, and including the hidden debts of Public-Private Partnerships.

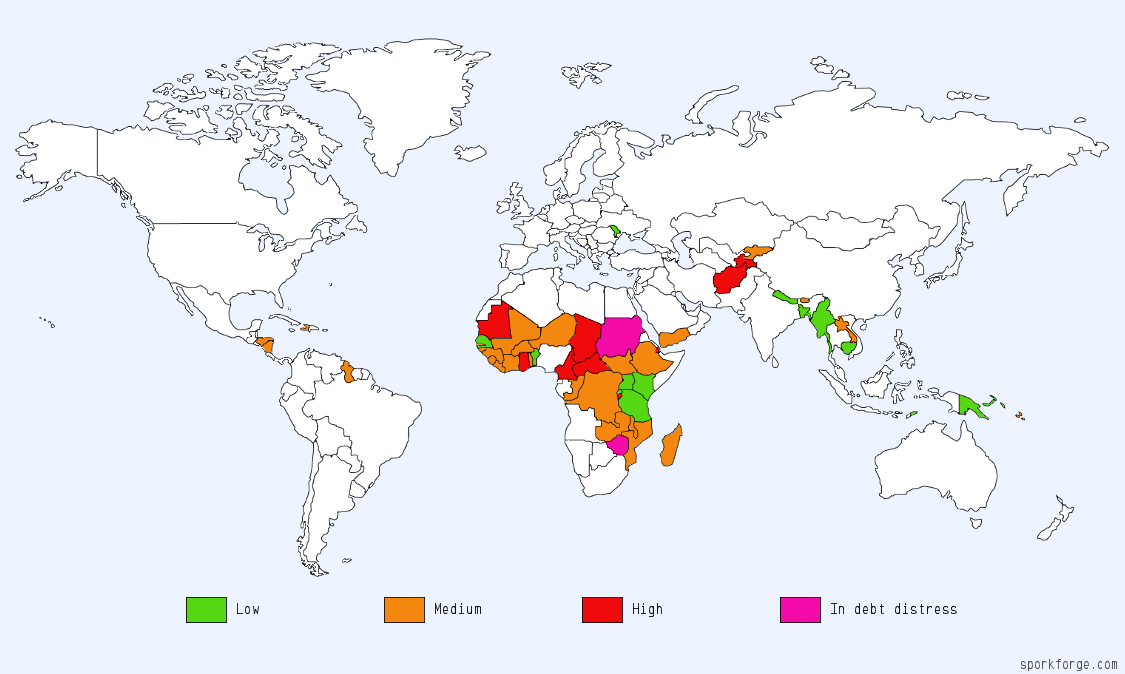

The IMF and World Bank Debt Sustainability Assessments rate countries as at low, medium or high risk of not being able to pay their debts, or ‘In debt distress’ where governments have defaulted on some external debt payments.

Of the 67 countries currently with a rating, 13 are judged as at low risk, 36 at medium risk, 15 at high risk and three as in debt distress. These assessments are used to decide whether and how much loans should be available from various institutions. For instance, the World Bank, African Development Bank and Asian Development Bank are meant, under their own policies, to give all loans to low risk countries, a mix of half loans and half grants to moderate risk, and all grants to high risk and in debt distress countries.

The IMF and World Bank conduct the assessments, yet they themselves are major lenders. Just over 40% of external debt owed by low income country governments is to the IMF and the World Bank. This is a clear conflict of interest. For instance, the IMF and World Bank have an incentive to be overly positive about the debt prospects of countries which are large borrowers from them and have closely followed their economic policies. In contrast, the IMF and World Bank also have an incentive to be overly negative about the debt prospects of countries which have ignored their ‘advice’.

One way this bias is seen is that the financial costs of World Bank promoted Public-Private Partnerships are not included in the Debt Sustainability Assessments. Many Public-Private Partnership schemes follow a UK designed model, where private companies are guaranteed payments over a specific proportion of time in return for building infrastructure. This has kept the debt off the books and out of assessments. In contrast, if the same investment had taken place through government borrowing, it would be fully included.

Another is that the assessments seek to reinforce the IMF and World Bank’s ideological bias in favour of policies such as trade liberalisation, deregulation and VAT being the main source of tax income. Governments implementing such policies are more likely to get a ‘lower risk’ rating.

The current debt analyses focus on whether or not a government can continue to pay. The history of the last 40 years is that governments tend to continue to pay debts for too long after they have become a large drain on resources, leading to economic stagnation and increasing poverty through cutting social spending rather than debt payments. The statement instead calls for assessments to be based on whether or not debt is preventing the meeting of the Sustainable Development Goals.

Debt crises have had negative impacts on people in countries on all continents at all income levels, from Ghana to Greece, Argentina to Zambia. Yet the current detailed assessments are only conducted for a range of 67 impoverished countries. The IMF’s debt assessments of other countries do not have any risk rating, nor do they have detailed information on key indicators such as debt payments as a proportion of government revenue or exports. The statement calls for assessments to be conducted for all countries, not for low income countries to be singled out.

The ten changes the organisations call for are:

- Make assessments independent

- Base them on the Sustainable Development Goals

- Use them to help encourage useful, productive investment

- Stop including irrelevant criteria

- Make debt service to government revenue the most important indicator

- Include currently hidden liabilities especially from Public-Private Partnerships

- Include domestic debt but maintain distinction with external debt

- Conduct more work on external private debt

- Review stress tests

- Include all countries

The statement and full list of signatories is available here.